'Godfather of Effectiveness', Peter Field, says Keep Calm and Carry On.

Here's what advanced leadership really looks like. LinkedIn’s global think tank, The B2B Institute, which funds research into accelerating growth in the B2B sector, has commissioned the ‘All Weather Marketing’ series of data-driven essays with contributions from global experts, exploring the effectiveness of advertising during an economic downturn. The first article in the series is from B2B Institute Research Fellow, author, strategist and marketing consultant, Peter Field.

Executive Summary

As I write this, it looks increasingly certain there’s going to be a recession. It will probably be different to ‘normal’ recessions, but many of the lessons about advertising from previous recessions still apply:

- Continuing to invest in brand advertising is recommended (if resources are available) but there is a diminished role for short-term sales activation in the current crisis due to consumer demand patterns, with a few exceptions. Data from the 2008 recession shows the value of investing in brand.

- Featuring humanity and generosity in advertising are advised: the use of emotions and humor can be helpful.

- Demonstrating humanity and generosity through behavior is also advised: brands should ask themselves the question, 'how can we help?'

Keep Calm and Carry On

Even as we wait to discover just how great the impact of the COVID-19 virus pandemic is going to be on economic activity, it now looks almost certain that there will be a recession. Though governments will move heaven and earth to ensure that it is as short and as shallow as possible, the temptation for many in the business world will be to cut marketing and advertising costs to the minimum, especially if this is their first recession. The same uncertainty about what to do was evident in 2008, at the start of the Global Financial Crisis, when no one was sure how bad things would get and the natural temptation was to assume the worst. But is that the best approach? And can we learn anything from previous downturns that will help us weather this one and emerge stronger?

In this article, I have examined the IPA data from around 50 case studies covering the 2008-9 recession period: while limited, the data nevertheless reveals how different investment and strategic approaches performed then. The data source is the compulsory confidential data submitted alongside entries to the IPA Effectiveness Awards competition in early 2010. The data covers inputs such as advertising strategy and budget, and a number of business outcomes, such as share and profit growth, allowing us to form a view about how the former influences the latter.

Not a 'normal' recession

The first caveat is that what we face is unlikely to be a ‘normal’ recession: it will be the first disease-driven recession of the modern era. Already it is playing out in very unusual ways. As in most recessions, the effects depend greatly on the sector: people still have to eat and take care of themselves but can delay discretionary purchases. Already the difference between essential and discretionary purchasing looks like it will be much more pronounced than in previous recessions. Thus far, many essential categories have been characterized by elevated or even panic buying, not the more usual deferral or down-trading, so what should brands in these categories be doing?

The answer largely depends on how scalable the business is and how flexible its delivery. For most physical products and services, demand is exceeding the ability to supply, but scalable businesses delivering important needs to house-bound customers, such as TV stations and video conferencing platforms that are not dependent on workplace usage, are fortunate exceptions. They are enjoying – and meeting – bumper demand, so there is a strong case for these businesses to exploit short-term demand (by means of lead generation activity) to build long-term market share. Brand building and short-term sales activation both make perfect sense for these brands in the current crisis. For the many brands that are unable to meet demand, however, extensive use of short-term sales activation would make little sense. But, for them, does brand building at such a time make any more sense? Can continued brand advertising signal important reassurance? With appropriate sensitivity to the fearful state of most people, brand building may in fact be the best approach, as we will see.

"With appropriate sensitivity to the fearful state of most people, brand building may in fact be the best approach, as we will see."

The B2B impact

In some discretionary categories where revenues have fallen to levels that threaten the survival of companies, such as airlines and catering, there may be no choice but to cut all advertising to conserve cash. In these situations, where goods or services may not be deliverable, or customers non-existent, there is certainly no point in trying to attract short-term buying. But, if the resources are available, the arguments in favor of brand building are stronger. This may not be in the form of costly conventional advertising but could perhaps involve eye-catching initiatives that reflect the mood of the times. Already we are seeing acts of generosity and humanity by some companies – these are praiseworthy in their own right and help to support the morale of staff and stakeholders during the crisis. But these acts also help to keep the brands salient and hopefully create positive emotional associations that will prime or remind future purchasers when markets recover.

The effect on B2B markets will be complex, with many differing sector-specific patterns. In many cases, they will be as severe as the worst of B2C. As we have seen in China, now is not a good time to be a sub-contractor for a business serving discretionary consumer markets (e.g. automotive). With many employees now working from home, there is also likely to be a big impact on goods and services that support the workplace, unless they can pivot to support working from home.

"Now is a good time for these businesses to be building market share through a balanced mix of brand building and sales activation, assuming they can meet demand."

On the other hand, businesses supporting those that serve essential consumer markets, or the current colossal shift to working from home, are more likely to see smaller or even positive impacts. Now is a good time for these businesses to be building market share through a balanced mix of brand building and sales activation, assuming they can meet demand.

But for B2B businesses whose customers and prospects are unable to buy, or who cannot meet existing customer demand, pursuing bottom-of-funnel, short-term, sales activation makes little sense unless it can help shore up existing relationships. For these brands, investing in long-term relationship-building is a better path forward. For the many activation-focused B2B brands, this will necessitate quite a shift in strategy.

"Because the sales funnel in B2B purchasing is generally longer than in B2C, the arguments in favor of supporting long-term growth through brand building are likely to be even stronger in B2B than in B2C. B2B Brand associations created now are likely to bring the greatest sales benefit during the recovery period, precisely when the rewards are biggest. Brand advertising is not about profiting in recession, it is about capitalising on recovery."

Historically, most recessions last around a year, sometimes five quarters. Hopefully, this pandemic will not last long enough to extend the duration of the recession beyond ‘normal’. Pandemic-based downturns tend to be v-shaped and during the last 100 years most have lasted around a year, according to the Harvard Business Review. This means that when all restrictions are finally lifted there is likely to be an enormous collective release of pent up demand, something wise businesses will be prepared to service well. A sharp recovery would be a departure from ‘normal’ recessions of the past, so the lessons from past recoveries may need to be reconsidered given this is an unprecedented, disease-driven downturn.

Reconsidering Lessons from the Past

The lessons for the marketing profession from the 2008 recession in the UK, for example, were clear, but they may not apply fully to our current situation. So with that in mind, to what extent should those lessons apply now?

Lesson One: Focus on the Long Term

In the last recession, some advertisers cut brand advertising spend, assuming this to be prudent, and many established media saw advertising revenue fall by 20% or more. However, because this was also the early period of big data, online advertising revenue actually grew by about 20% in 2008. Overall, advertising spend held remarkably steady, but it was the start of a dramatic drift to short-term activation media, something that has cost businesses dearly over the years since then. The IPA Databank allows us to examine how the balance between long-term brand building and short-term activation influences the effectiveness of a campaign. In normal times, the IPA data argues for a balance between brand and activation spend in the ratio 60:40 for maximum business effectiveness.

"Most businesses today already spend less than 50% on brand-building – dangerously below our recommended 60% – so there is certainly no sense in cutting brand building further unless survival depends on it."

The IPA data on how campaigns balanced brand and activation spend was less extensive back in 2008, so there is some uncertainty in the findings, but the data suggests that a slight shift from the 60:40 optimum towards 50:50 might have been sensible in 2008. However, because of the highly unusual impacts of this pandemic, from panic buying in some categories to market shut-down in others, this is unlikely to be best practice during this recession. Short-term activation makes much less sense, when either demand cannot be met or simply doesn’t exist. And in any case, most businesses today already spend less than 50% on brand-building – dangerously below our recommended 60% – so there is certainly no sense in cutting brand building further unless survival depends on it. Either way, it looks like a greater focus on brand advertising investment rather than on short-term sales activation is more sensible from here on in. Certainly, businesses should resist the seductive sales pressure from short-term media to increase activation spend, unless they are one of the fortunate few countercyclical businesses that can meet demand.

Lesson Two: Defend Your Share of Voice

In 2008, some brands cut their Share of Voice (SOV – the percentage of category advertising expenditure spent by the brand), while others raised theirs. We know that SOV is strongly correlated to market share – if we allow SOV to fall below the brand’s share of market then market share is likely to fall over the year following. We therefore know that cutting advertising budgets – and SOV – during a recession is a risky strategy. It may provide some short-term relief to profitability (because costs are cut), but the subsequent loss of market share that follows will be extremely difficult and expensive to regain during the recovery. Thus, the long-term impact on profitability will be highly damaging and it is better to take the short-term profitability hit to maintain SOV and defend the brand.

"The good news for businesses that defend their brands is – because some advertisers will pull budgets thus reducing category ad spend – maintaining SOV is likely to be cheaper than in normal times."

The good news for businesses that defend their brands is – because some advertisers will pull budgets thus reducing category ad spend – maintaining SOV is likely to be cheaper than in normal times. Of course, predicting what SOV a given budget will achieve in a rapidly evolving media environment can be difficult, so defending SOV likely requires a highly adaptable approach.

Lesson Three: Seize Your Market Opportunity

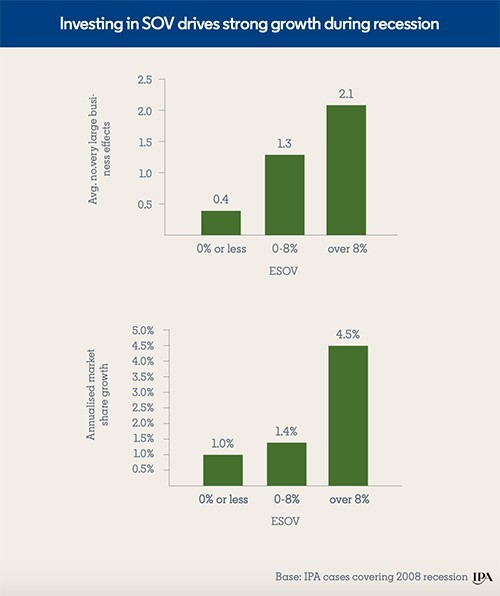

The implication of falling SOV costs is that recessions can be a low-cost growth opportunity for brands. But in this recession, we can also add the opportunity presented by a house-bound population’s growing usage of media such as TV, social and online news channels. We saw in 2008 that the brands that took advantage of lower SOV costs to boost their SOV achieved impressive business gains. The following charts examine three equal-sized groups of cases from the 2008 recession with different media investment strategies measured by Excess Share of Voice (ESOV) — the difference between a brand's share of voice and a brand's share of market — the key measure of investment. Group one, whose ESOV was zero or less were at maintenance levels or lower, but were still advertising (i.e., they had not gone ‘dark’). Group two had modest growth levels of ESOV in the range 0-8%. Group three saw the recession as an opportunity, with over 8% ESOV. Remember that some of these brands will have merely held their spend level to achieve this level of ESOV. That said, the brands that invest in ESOV saw 5 times as many very large business effects (such as profit, pricing, share, penetration etc.) and 4.5 times the annual market share growth.

The impact of long-term profit growth (measured in these case studies mostly after the end of the recession) clearly shows why taking the short-term hit to profitability, by investing in advertising during the depths of recession, is ultimately worth the long-term profit.

Add to this the general finding that stronger brands are more resilient to adverse events, and you have a fairly compelling argument for investment.

What is certain from the 2008 experience and earlier recessions is that 'going dark' by pulling all brand advertising brings the real risk of permanently weakened business performance. It is sensible to debate the tone and nature of brand advertising to recession-hit customers, but not the importance of it.

Lesson Four: Demonstrate Humanity and Warmth

The appropriate tone of advertising in this recession may be different from previous ones and may change over time, so we need to keep a close eye on the live guidance provided by continuous market research studies. In this crisis we are not yet dealing with an elective decline in consumption but an enforced one that, at least for the time being, has implications for the tone of advertising. A broad group of marketers have expressed concern that continuing to advertise as usual might risk alienating consumers. Market research company System1, who measure consumer response to new ads on a daily basis in the US and the UK, are not yet seeing any signs of “ad alienation” (as of April 2020) due to the introduction of social distancing. Put another way, people are not changing previous buying attitudes, they are simply prevented from exercising them. So, early research findings appear to suggest that fears about continuing to run existing advertising may be overstated.

"Early research findings appear to suggest that fears about continuing to run existing advertising may be overstated."

This may change in time if the recession is deep and long enough, but because the most likely shape of recession is relatively short but sharp, we shouldn’t yet fall into the recessionary advertising mentality seen in 2008. This was characterized by a shift away from purely emotional advertising as advertisers felt more serious approaches fitted the mood of the people. The IPA data suggests that there might have been some limited justification for this in 2008, to the extent that campaigns that supported emotional platforms with rational content appear to have enjoyed improved effectiveness, but this is from a base of low effectiveness in normal times. In fact, many of the most celebrated effectiveness case studies of that time were emotional feelgood campaigns – albeit rooted in the reality of what the brands did for customers, rather than abstract emotional ‘wash.’ Examples include Heinz, T-Mobile, Virgin Atlantic, Hovis Bread and Cadbury.

A couple of sentences from the T-Mobile IPA case study are worth revisiting now: “Our research showed that people’s deeper human values were coming more to the fore. As the recession bit, people were responding in kind – literally – by turning to friends and family with warmth and good humor where we might have expected angst and despair.” T-Mobile built this insight into their highly effective campaign during the recession.

It is too early to tell whether the mood of populations will turn against ‘business as usual’ advertising, but for the time being we should expect the key virtues of emotional advertising to hold true even during recession: priming long-term buying of brands more powerfully than rational advertising, making a bigger impact on price sensitivity, and reducing pressure on pricing. So long as the emotional platform is sympathetic to the prevailing mood, the arguments for consistency probably outweigh those for change.

This in no way undermines the value of highly topical opportunities to build goodwill through acts of humanity and generosity. This recession is unusual in that having a common enemy – COVID-19 – has generated a level of community spirit (toilet roll panic buying aside) that far exceeds that seen in previous recessions. If people are demonstrating solidarity in adversity, then brands doing the same thing will earn their respect. Many farsighted companies have willingly offered free goods and services to mitigate the emergency or to shield their employees from insecurity. Others have behaved less well so far. It doesn’t take a psychologist to unravel who will benefit most in recovery.

Guidance for this Recession

So, here are seven guidelines derived from adapting previous lessons to this very new situation:

- Do not hit the panic button and withdraw brand advertising, unless short-term survival depends on it.

- Resist the pressure to switch advertising spend from brand solely to activation – it makes very little sense to do so, even in the short term. Customers, in many cases are not reluctant to buy, they are unable to buy.

- If the resources can be found, aim to maintain your share of voice, ideally at least at the level of your market share, where SOV equals SOM. You may even be able to reduce your budget if others are cutting theirs but be ready to adapt quickly to developments. You will need to monitor competitive activity regularly.

- If the resources can be found, consider the opportunity to invest in lower-cost long-term growth by increasing share of voice during the recession.

- Do not abandon your existing brand campaign unless it is clearly unsympathetic to the mood of customers. There may be more value and reassurance in continuity than in change.

- Do not be frightened to use emotional brand advertising during recession – but ensure it is appropriate to the mood of customers. System1’s live research findings are right now supporting the use of advertising that demonstrates humanity through warmth, generosity and humor.

- Look for tactical opportunities to create goodwill through acts of humanity and generosity, especially if you were proclaiming these virtues before the emergency.

The coming months will test everyone – we are in uncharted territory. But this was much the same in 2008 and it was the brands that held their nerve – and share of voice – that bounced back strongly when recovery came.