'The revenue declines at Snap, Twitter, Facebook, even YouTube are down to retailer media' - who's next?

An Mi3 editorial series brought to you by

Coles 360 and Resolution Digital

Jack Myers: "Facebook, Google have benefitted over the last decade from having their own first party data. Now brands are looking at the availability from their retail partners of first party data. It’s only natural that they are going to connect it."

An Mi3 editorial series brought to you by

Coles 360 and Resolution Digital

Mi3 Special Report:

Retailer Media Next

Expert analysis & market impacts for brands, publishers and agencies.

Data compiled by US analyst Jack Myers suggests tech platform revenues are being hit hard by retailer media’s rise – and the softness in TV markets is no coincidence. Australian market dynamics differ, but Citrus Ad founder Brad Moran reckons Coles and Woolworths “could dominate the entire ad market if they wanted to”. Agency execs think search and social have more to worry about than TV networks. But some experts think the looming privacy overhaul – and ensuring compliance costs – may curb some retailer enthusiasm to monetise loyalty data via retailer media networks, while blowing a hole in the economics of loyalty programs themselves.

What you need to know:

- US retailers now seriously eating into search and social ad budgets, with TV networks now seeing first real wave of impact, per US analyst Jack Myers.

- But senior agency execs in Australia think the TV networks are insulated – with BVOD actually primed for growth as retailers harness shopper data to power targeted buys. They think search and social channels have most to lose.

- While Woolworths and Coles “could dominate the entire ad market if they wanted to”, per Citrus Ad founder Brad Moran, others forecast a boom in retailer media networks and a cross-sector retail push to monetise customer data due to high margins.

- But some experts think Australia’s privacy law overhaul – even before details have been finalised – may have significantly curbed enthusiasm.

The losses that we’re seeing now in several of the major digital platforms, whether they be Snap, Twitter, others … it’s money shifting to the retail media category for the first time this year.

US-based ‘media ecologist’ Jack Myers told Mi3 that industry data compiled by his firm, Media Village, shows digital retailer media – separate to legacy shopper marketing and sales promotion spend – is currently a circa $25bn business in the US. In 2022 it grew 20 per cent, per Media Village data, as major retailers become increasingly sophisticated – and competitive. That curve is accelerating: By 2025, he predicts digital retailer media will stand at $50bn with the money coming out of TV networks and social media platforms.

“The losses that we're seeing now in several of the major digital platforms, whether they be Snap, Twitter, others; the flat reporting that we're seeing at Facebook, Google, even YouTube are being heavily attributed to TikTok, which is certainly the case. But more so, it's money shifting to the retail media category for the first time this year,” said Myers.

“Take YouTube out of that bucket, because I believe YouTube has a whole other set of sophisticated understanding of the unique marketplace that they have. And take TikTok out of the equation for now, because it is the latest hotspot. But Facebook, Snap, Twitter, keep going … I believe they've lost their way. I believe they fundamentally don't know what their business is anymore. They're riding on the coattails of their prior business models. Their leadership is increasingly distanced from the marketplace.”

He suggests TV networks are feeling similar pain.

“We're seeing a real softness in the US network television upfront marketplace and in the continuing scatter markets [where advertisers hold back-upfront dollar commitments in a bid to get better value closer to real-time],” said Myers.

“Much of that is also being attributed to TikTok. But my data shows that it is flowing for the first time from national television into retail media categories.”

Aggregation: Next wave?

While locally some suggest retailer media will be a race for scale, Myers thinks aggregation will be the next wave, putting further pressure on publishers.

“We're beginning to see a move toward the major demand side platforms, companies like The Trade Desk, Magnite and others … to develop collective retail media – aggregated retailers, smaller retailers coming together in a programmatic model to support retail media initiatives,” predicts Myers.

“It's realistically two to three years away, but I believe that will be a wave that has significant impact on legacy media. The reality is that legacy media, at least here in the US, has yet to wake up to the competitive threat from retail media. They're attributing it to almost everything but the real cause of softness and stagnancy in the marketplace.”

The collapse of the funnel

Myers thinks that increasing involvement of procurement departments within media allied with demand for hard results beyond reach and the increase in first party data are key drivers in the “exponential” rise of retailer media.

“Companies like NBCU, Facebook, Google have benefitted over the last decade from having their own first party data. Now brands are looking at the availability from their retail partners of first party data. So it’s only natural that they are going to connect their marketing dollars to actual sales.”

Hence, he says, “the funnel is imploding”.

“The idea of advertising as an awareness vehicle, that pool or that pie is shrinking and the bottom of the funnel pie is growing. Marketers can come in at any point to the funnel now and have first party data to help guide their decisions.”

When people talk about 'retail media' and the size of the industry, it's just like [bucketing together] 'advertising in CPG world'. It's literally that broad because they encompass so many verticals. It is very, very hard to understand how much has actually been generated from what Citrus calls retail media.

On network, off network: Confused definitions?

“Retailer media is spoken about a lot a the moment. But ask ten people its definition, and you’ll get ten different answers,” says Brad Moran, who founded retailer media ad platform CitrusAd six years ago in Australia and sold it to Publicis for north of $200m in 2021.

While McKinsey has forecast huge growth, US$100bn in spend in the US alone by 2026, with eMarketer predicting US$55bn in US retail media ad spend by 2024, Moran suggests those figures could be misinterpreted. He’s keen to “debunk a couple of myths”. Much of the money bracketed as ‘retailer media’ in the US does not accrue to retailers that have set up media businesses, per Moran. It’s going to Amazon, which posted global ad revenues of US$37.7bn for calendar 2022.

“What many people probably don't realise is how much of that money is spent off Amazon.com,” says Moran. “Amazon’s ad network spans millions of websites. Most of its ad money comes from retargeting offsite shopper discovery.”

That creates “a story that retail media is massive, it's growing,” says Moran, which is useful for CitrusAd’s own growth ambitions, and those of retailers globally and locally. “But when you think about actual onsite sponsored products and banners, if you just carved that part of Amazon business out, it would be substantially smaller.”

Under Publicis, Citrus is partnered with data unit Epsilon, which Moran suggests offers an illustration of the revenue ratio between on network (media assets owned by retailers and bought by brands) and off-network (using retailer data to power targeted ads around the web).

“To give you an idea of how big the offsite component is to the on site, the average customer for us, Epsilon would probably do 25-30 times the revenue that we would.”

“So when people talk about retail media and the size of the industry, it's just like [bucketing together] 'advertising in CPG world'. It's literally that broad because they encompass so many verticals. It is very, very hard to understand how much has actually been generated from what Citrus calls retail media, which is money spent directly between a brand and a retailer,” says Moran. “But that bucket of money is very different to what a lot of the reports say.”

US market: consolidation ahead

Moran agrees with Media Village’s Jack Myers on the trends of consolidation and aggregation. In the US, most retailers have realised they can’t compete alone, which is why Citrus has been able to attract 21 retailers to its ad network, with a collective grocery reach Moran claims “is now bigger than Walmart and Amazon”.

“When you talk to Nestlé or Unilever, whoever's advertising, it's one portal, one point of contact for $300 billion worth of sales, that's the attraction,” says Moran. “The retailers know a $5bn business in the US does not get to meet the head of marketing at P&G. They get the local guy, the local budget and they don't really grow. So if you want to compete on a national scale with national budgets, you need national size, which collectively they form.”

From a tech perspective, Moran sees consolidation underway as US retailers seek cost efficiencies by pushing media operations established in-house, and the related risk, “back onto full service providers and technology players”, with many seeking one-stop shops. Should that trend continue, with procurement increasingly leading RFPs, Moran thinks it may ultimately favour the “the big conglomerates with big product stacks” to bundle.

“So macro level, I think consolidation of tech is now key. Even just looking at our roadmap, the number one thing we’re building out is our API. We have an API for connecting to retailers, but we want to build out a Shopify-type app store. There are now so many small pieces of retail tech that you simply can’t build them all. [Retailer media] needs to be frictionless. So there is a lot of opportunity to enable that.”

There is a big category job to do in measurement.

Double digit growth, but FMCGs shopping around

Year-on-year, Moran forecasts “12-15 per cent growth” for mature US retailer media businesses. While that is below market-wide forecasts made by the likes of McKinsey and other US analysts, Moran says FMCG brands are now “looking at their budgets more delicately and seeking best bang for their dollar.”

Metrics challenge looms

The rise of retailer media is creating a measurement challenge for brands. Because there are no unified standards, advertisers are facing a patchwork of different reporting methodologies. The issue is thorny in the US, with the likes of Unilever urging retailers to align. Australia will face the same problem if multiple retailers launch media businesses. “There is a big category job to do in measurement,” per Zitcha’s Troy Townsend.

US marketers feel retailer pressure, search budgets shifting

US peak advertiser body the ANA polled members ahead of a retailer media deep dive released in January. Key findings are that 56 per cent of advertisers are working with five or more retail media networks (RMNs) but that many are concerned that they are not driving brand growth. Fully 85 per cent of marketers polled said they feel pressured by retailers to spend with RMNs and the report found that retailer media spend is not incremental, but pulling from existing budgets – shifting the balance of investment from brand to short-term sales. Measurement transparency and lack of standardisation were standout issues, but overall, marketers were optimistic about retailer media: Within two years, 58 per cent expect to be using more RMNs than they are today, and 73 per cent expect to be spending somewhat or significantly more on RMNs than they are today.

According to the report, 80 per cent of advertisers said paid search is the most important tactic offered by RMNs, followed by on-site advertising. Per one advertiser interviewed for the report: “Sixty per cent of all searches today are starting on commerce sites. Traditional paid search is kind of a waste.”Coles and Woolworths could dominate the entire ad market if they wanted to.

Australian outlook: Growth, fragmentation, trade-marketing realignment

Sizing the Australian retailer media market is an inexact science – because current revenues are predominantly trade budgets and far harder to compile than traditional media or ad spend. PwC last year estimated Australia’s retailer media market stood at $850m in 2022, forecasting revenues to hit $2bn by mid-2025 in its central forecast.

What is clear is that Australia’s media landscape faces further fragmentation as the big two supermarkets accelerate media businesses. As Citrus Ad’s Brad Moran puts it: “Coles and Woolworths could dominate the entire ad market if they wanted to.”

Verticals including pharmacy, homewares, garden, consumer electronics, financial services, fashion and beauty are also entering the market vying for a larger slice of trade – and marketing – budgets from brands.

Cartology is aiming to increase its lead, buying up Shopper Media’s network of screens last year, bringing Big W into the fold and this year pushing into shopper-data-powered BVOD buying via a partnership with Liveramp. It’s also positioning to sell media to non-grocery brands.

Coles has built an integrated retailer media unit and while this year is focusing on trade suppliers, plans to push harder into agencies and marketing budgets from next year on.

While stating they expect the majority of revenue – and higher margin – from on-site media (i.e. their digital properties and in-store), both supermarkets are cognisant of Amazon’s off-network growth in the US and its relative weakness in the Australian market versus their 70 per cent share of the grocery market and huge loyalty data.

What I do see is far greater working between marketing, commercial development and sales on the customer journey, full end-to end planning [due to retailer media and ecom more broadly] … That is a fundamental shift we are making in our business.

Marketing-trade overhaul, ROI questions

FMCG and drinks marketers interviewed recognise the value of tapping retailer and loyalty data to target customers. (Roughly eight in 10 Australians are signed up to a supermarket loyalty scheme.) But they want proof that retailer media moves the needle via sharper, more consistent measurement and deeper reporting and analysis.

Retailers must hold themselves accountable to the same standards as other media in terms of robust measurement and reporting, per Nestlé marketer Anneliese Douglass.

PepsiCo CMO Vandita Pandey takes a similar view: the retailers’ pipes and wires aren’t yet sufficiently robust. “We’ve got quite a bit more runway and learning before we would see a significant increase in investment.”

As v2food Marketing Director Jade Lish puts it: “Retailer media is really important for us,” but the supermarkets would take more of her budget “if they could show me the data.”

But Nestlé’s Douglass said a “fundamental shift” is underway as the FMCG giant more closely aligns marketing, sales and commercial development teams as a result of retailer media and ecom dynamics. Across the broader market, trade-marketing realignment is yet to play out, but structural change may lie ahead if Australia’s retailer media growth curve mirrors that of the US.

We’re seeing more spend being diverted across retailer media and we are seeing it deliver ROI. The challenge will be as the landscape becomes more competitive, costs will naturally increase, and that will put pressure on ROI.

Price inflation, clutter

Other marketers are starting to notice increased clutter – and higher prices – as retailers add inventory to their media platforms and brands compete for top spots. “Generic search terms [within retailer media platforms] are getting really expensive,” because brands want to be “in the right format on page one,” per Moccona Marketing Manager Aaron Wall.

Competition could alter those dynamics in some sectors. Resolution Digital’s Mohammad Heidari Far says Endeavour Group’s switch from Citrus Ad to Microsoft’s PromoteIQ platform saw ROI increases “from five to one to 15 to one”, though he acknowledged there will likely be a rebalancing as platforms mature.

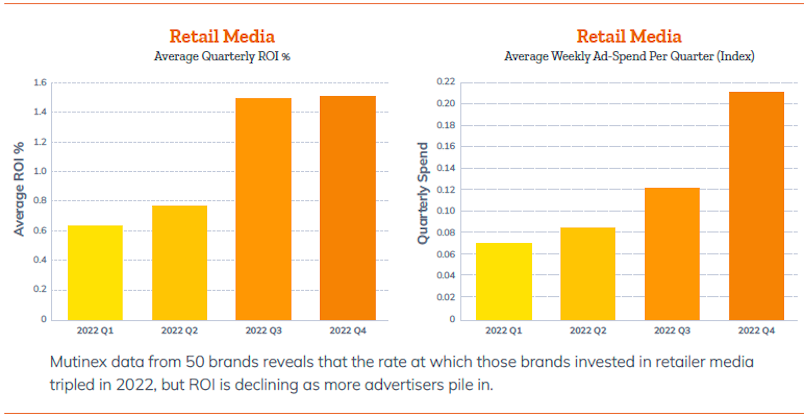

ROI plateau ahead?

Other data implies retailer media channels may already be seeing ROI starting to plateau as advertisers pile in. Henry Innis, Global CEO at marketing analytics firm Mutinex predicts Australia’s retailer media players will increase their revenue by “50 to 100 per cent” this year, but incoming advertisers will inevitably see lower bang for buck.

“We’re seeing more spend being diverted across retailer media and we are seeing it deliver ROI,” says Innis. “The challenge will be as the landscape becomes more competitive, costs will naturally increase, and that will put pressure on ROI: Early movers into a highly effective medium can access the inventory at far cheaper prices, but as the market normalises, ROI will generally normalise correspondingly,” he adds.

“So longer-term the market is unlikely to generate the huge returns that it has seen to date, in line with any maturing medium. We are probably just coming to the start of that cycle with retailer media,” suggests Innis.

We know it drives sales, retailers have good data sets to prove that. The question when we talk to clients is, ‘is it driving growth?’ Because that’s not the same thing.

Which publishers lose?

Media Village data suggests strengthening headwinds in the US market for linear TV, declines for search and a slowing of social media’s growth as retailer media rises. Those trends may follow in Australia, according to industry execs.

Omnicom Media Group Chief Investment Officer Kristiaan Kroon suggests Google will take a hit as retailers take search budgets. He thinks the large FMCG retailers face challenges in taking a greater share of upper funnel brand budgets: “[Retailer media] is weighted to performance. It’s not black and white, there are brand budgets in there and [brand] is a space that retailers believe they can grow into over time. But it’s a big challenge for them to meet.”

Zenith Digital & Data lead Joshua Lee thinks all social channels are at risk, but thinks Facebook in particular may face challenges if it is seen to underperform.

Whereas Youtube delivers both upper and lower funnel, he says Facebook can struggle, “and that’s when budgets can get squeezed a little. Especially for clients that don’t have the infrastructure set up, such as the Facebook conversion API,” says Lee. “So they might just look to increase retailer media spend.”

Resolution Digital Chief Product Officer Mohammad Heidari Farr says any performance channel is at risk if retailers can better close the loop. But he also thinks retailers’ own legacy trade channels will be cannibalised by digital. “So I think we will see more discounting being added to some of the traditional channels and inventory types. Hence brands can extract more value from those channels and shift it into digital, because it is more measurable and closer to ROI,” says Heidari Farr.

BVOD, however, could benefit as retailers apply loyalty data and push further into off-network business models, increasing demand and prices for BVOD publishers. Likewise retailer data-powered programmatic digital out-of home – which presents both a demand opportunity and a supply threat to OOH publishers, with the likes of Cartology now a significant screen owner following its acquisition of Shopper Media.

Some OOH publishers are taking countermeasures. oOh!Media has rebadged its retailer-focused operation and is looking to partner more deeply with retailers, while Westfield owner Scentre Group is understood to be developing a strategy for market entry.

If an FMCG brand operates trade marketing and brand marketing separately, it’s quite difficult for agencies to bring that together.

Agency-brand implications

Media agencies do not usually interact with trade teams, where big retailers are currently focusing the vast majority of their business. Marketing departments are also adjacent to the action. That could cause tension – and Coles 360 strategy lead Sam Hegg thinks structural change is required. “If an FMCG brand operates trade marketing and brand marketing separately, it’s quite difficult for agencies to bring that together,” says Hegg. “Where we’ve seen holistic structures within FMCG brands, the benefits come quite quickly.” Coles 360 GM Paul Brooks agrees: “If FMCGs do that, agencies will align themselves.”

Some brands have taken the plunge – with Goodman Fielder last month handing responsibility for its trade marketing budget to media agency Initiative.

We have to create bucketloads more content. You go from one version to thousands.

Retailer media: Who’s next

Which retailers launch media businesses next is “all down to their approach with their data,” per Resolution Digital’s Mohammad Heidari Far. “Home and garden has got huge potential. But from a readiness perspective, I think fashion and beauty are really interesting,” with Adore Beauty the latest to move.

He says Resolution Digital is advising four retailers on how to build their own media network. “From the level of maturity of those conversations, I am hopeful that some of them will come to market in 2023,” he says. At the top end, he thinks Wesfarmers’ loyalty play, OnePass, could ultimately lend itself to a major media play, if the group can make it work. Heidari Far predicts growth across the piste because many retailers are now viewing media as a defensive position to avoid losing market share.

Content implications: Automation or bust

Retailer media is driving significant increases in content requirements, per Justin Ricketts, ANZ CEO at Hogarth Worldwide, which provides digital production for Woolworths. “We have to create bucketloads more content,” says Ricketts. Throw in multiple channels, retailers, day-part, weather and economic data, and “you go from one version to thousands”. He says automation is the only solution – with AI-powered optimisation already in play. The next step is getting AI to predict which retailer ads will perform – and why – and ultimately make the ads without human intervention, “and that is only months away”.

[The biggest privacy compliance costs will fall on those] making the most money out of loyalty data … those with the biggest databases that they are trying to convert into media channels, because their business proposition is based on getting data and permission. They didn’t need permission before, now they do.

Privacy overhaul: Limiting factor?

After Optus and Medibank’s privacy breaches, brands are “very concerned” about anything related to customer data, per Yahoo’s Apac data chief Dan Richardson. He thinks that could be the biggest brake on retailer media and monetising retailer data. “[Retailers] have to work through a lot of privacy and security risk compliance to even get to a point where they can think about launching a media network,” says Richardson.

That nervousness has since been compounded by Australia's sweeping privacy overhaul.

Published late February, the proposed reforms significantly tighten consent requirements around how customer data is used and bring de-identified data – and geo location data – into scope. Customers must be told in very simple language how their data will be used – and whether it will be used for purposes such as targeted advertising or marketing. If data is shared with third parties, that will require explicit opt-in consent. Use of geo location tracking and targeting will also require a specific opt-in, which has implications for shopping centre and retail screen networks.

The proposed law changes also outline a significant strengthening of penalties – with regulators being given greater powers to proactively find and investigate privacy breaches and misuses of data, and criminal charges for repeated breaches.

Consumers will also have the right to opt out of targeted advertising and if they do not consent for their personal data to be used, businesses will not be allowed to deny them services.

If passed, those proposals could throw the economics of loyalty programs into question – and loyalty programs often underpin retailer media.

Meanwhile, opt-in consent for third party data sharing could prove problematic for retailer campaigns that use shopper data to target their customers across the open web, i.e. off network retailer media activity.

Loyalty: Opt-outs bust economics?

“The proposals allow customers to participate in loyalty programs but opt out of being targeted, which means the loyalty programs that are essentially marketing channels in disguise will have to be much tighter in seeking permissions,” says Tim Tyler, Managing Partner at specialist loyalty consultancy Ellipsis.

What’s more, loyalty operators will have to allow members to delete data. “I’m not sure they will be happy with members that opt out of targeted ads and ask them to delete data,” says Tyler. “All of a sudden, that value proposition is no longer there.”

There are two “loyalty worlds”, per Tyler – the contractual and non-contractual. One has the privacy proposals largely covered, the other probably doesn’t.

The former applies to the big players, such as banks, which operate “where customer identity is already known and the value exchange is paying for tenure of wallet and paying for share of data. Because the bank already knows who you are and where you spend – and the reputational damage if privacy is violated in the banking environment is already real,” per Tyler.

“In the non-contractual environment, where customers are anonymous and loyalty is established to get identity and enable tracking, the proposals are more impactful – because if a customer asks to delete their data, you no longer have the means of recouping your outlay.”

Supermarket sweep

Tyler thinks the biggest compliance costs will fall on those “making the most money out of loyalty data … those with the biggest databases that they are trying to convert into media channels, because their business proposition is based on getting data and permission. They didn’t need permission before, now they do.”

Will that make retailer media more expensive? “Yes, potentially. But what we don’t yet know is how interested the Australian public will actually be. The Europeans haven’t seemed that interested. Not many are opting out [via GDPR].”

Do Australia’s proposals put the brakes on the post-cookie rush to build out loyalty programs? No, suggests Tyler. “But [loyalty operators] will have to get much sharper in proving the value of targeting … And compliance cost is the biggie – because there are enough activists in the community to make sure that the legal recourse is real.”

A version of this article was published in Mi3's Retailer Media Next report. Download it below.

Mi3 Special Report:

Retailer Media Next

- Australia's surging retailer media market unpacked - and where it's headed next.

- Implications for brands, budgets and the broader market.

- In-depth interviews with 25-plus marketers, retailers, platforms, agencies and analysts.

- Supported by Coles 360 and Resolution Digital.

Australia's surging retailer media market unpacked - and where it's headed next.

DOWNLOAD THE REPORT HERE